Companies can also hold shorter term T-bills themselves, if they want to avoid the risk of bank failure. Obviously that doesn't work for covering day-to-day expenses like payroll because they're not totally liquid, but for anything that you're not using for 6-12 months, it's totally viable.

Worth noting here that their losses were mostly not "bad" bonds per se in that the bonds they bought haven't defaulted. In fact they're mostly US treasury obligations. But when their deposits left they had to raise money, and since interest rates have gone way up the value of their bonds has gone down (bond prices move inversely to interest rates). It's not a big problem if you don't have to sell, but if you need the money to pay back depositors then you have to take the losses and they didn't have enough equity to cover the hole.

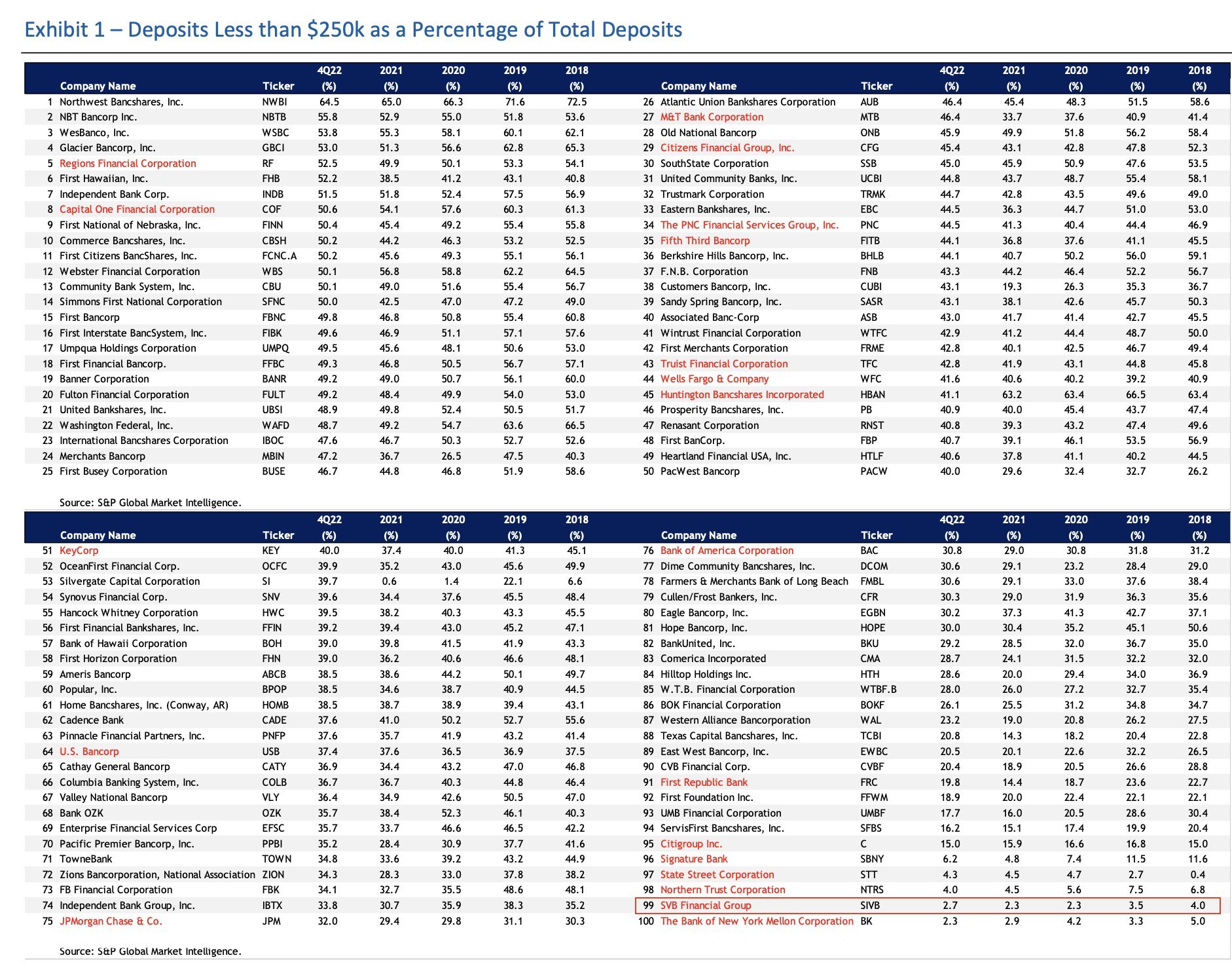

All the banks in the US have exactly the same issue, and they aren't required to mark held to maturity bonds to market price unless they sell them. The ones whose deposits are checking accounts and CDs from millions of people are probably safer than the ones whose deposits are all from venture backed startups.

I dont have time at this point to do a full rundown, but youve hit on a chunk of the issue here. The banks and financials were pushed buy high quality liquid assets. Thats what SVB did, and from that risk management perspective, they were good. Then rates rose in 2022 and its a massive problem because those assets are worth a lot less than last year. The. You have the bank run, where they have to liquidate these assets and obviously thats not ideal.

My concern isnt whether the extent of SVB is known, but its that theyre not the only one. Its unfathomable that there arent a lot of other banks in this similar situation, where theyre not invested in crazy securities, but the rising interest rate has hammered those prices.

So, what happens next week? Hard to say. But there are some difficult choices to be made on a few fronts, and a lot of uncertainty.

I don’t have time at this point to do a full rundown, but you’ve hit on a chunk of the issue here. The banks and financials were pushed buy high quality liquid assets. That’s what SVB did, and from that risk management perspective, they were good. Then rates rose in 2022 and it’s a massive problem because those assets are worth a lot less than last year. The. You have the bank run, where they have to liquidate these assets and obviously that’s not ideal.

My concern isn’t whether the extent of SVB is known, but it’s that they’re not the only one. It’s unfathomable that there aren’t a lot of other banks in this similar situation, where they’re not invested in crazy securities, but the rising interest rate has hammered those prices.

So, what happens next week? Hard to say. But there are some difficult choices to be made on a few fronts, and a lot of uncertainty.

Agreed. They certainly would have been pushed to buy quality securities, which Tbonds certainly are. However, they could have sacrificed some short term income in 2020/2021 and bought 2 year paper instead of 10 year paper, and then we wouldn't be having this conversation because they'd still be earning a spread on all of Roku's extra corporate cash...

There's also never just one cockroach, so I'd expect to see more come to light in the next little bit. Sometimes that is a self-fulfilling prophecy, as corporate treasurers just got a lot more picky about where they're keeping their extra cash as a result of this.

Yeah, that bank's average remaining bond duration was over 6 years which seems crazy given who they catered to. They assumed that withdrawals wouldn't exceed their bond maturity pace, but they bet wrong.

I also wonder if the removal of the Dodd-Frank Act in 2018 played a part in this. Before it was removed, smaller banks (sub $250B like this one) were subject to federal stress testing and had higher cash reserve requirements to mitigate shocks.

Yeah, that bank's average remaining bond duration was over 6 years which seems crazy given who they catered to. They assumed that withdrawals wouldn't exceed their bond maturity pace, but they bet wrong.

I also wonder if the removal of the Dodd-Frank Act in 2018 played a part in this. Before it was removed, smaller banks (sub $250B like this one) were subject to federal stress testing and had higher cash reserve requirements to mitigate shocks.

Well fixed-income 101 is literally duration management, so regardless of the regulation, anyone prudent should be managing that risk!

Yeah, that bank's average remaining bond duration was over 6 years which seems crazy given who they catered to. They assumed that withdrawals wouldn't exceed their bond maturity pace, but they bet wrong.

I also wonder if the removal of the Dodd-Frank Act in 2018 played a part in this. Before it was removed, smaller banks (sub $250B like this one) were subject to federal stress testing and had higher cash reserve requirements to mitigate shocks.

I read one piece that said they were a major lobbyist for the move from $50B to $250B, as a >$200B but <$250B bank they were one of the biggest beneficiaries of that change. Of course, then they aren't to big to fail so the Fed let them go down...

Well fixed-income 101 is literally duration management, so regardless of the regulation, anyone prudent should be managing that risk!

Every bank in the history of banking has a duration mismatch though. Borrow short lend long is the business model, and generally it works fine. The issue here (imo) is the scale - the liquid part of their balance sheet that was supporting the short term deposits shouldn't have been in 10 year paper. Having their equity in 10 year paper (or even 30 year loans) isn't an issue, but having demand deposits backing long duration assets is an issue, especially given the lack of stickiness in their deposit base. If they had sold a few $B in 5 year CDs when they bought those bonds this would probably also have worked out.

Well fixed-income 101 is literally duration management, so regardless of the regulation, anyone prudent should be managing that risk!

Might be explained by them not having a Chief Risk Officer for most of 2022:

Quote:

Silicon Valley Bank, a lender that was a fixture in the venture capital space for decades, collapsed on Friday. The California Department of Financial Protection and Innovation closed SVB and named the FDIC as the receiver. The trouble started on Wednesday after SVB suddenly announced a plan to raise billions in capital to cover big losses, setting off widespread panic among investors and the tech founders they backed. Shares of the company fell by around 60% in Thursday trading, another 20% in aftermarket trading, and were halted at the open on Friday. Hours later, amid reports that SVB was struggling to attract buyers in a sale, the government took control. In the run-up to all this, SVBs proxy statement, filed earlier this month, reveals that the firms chief risk officer stepped away from her role early last year, and the bank did not hire a replacement until this past January.

Every bank in the history of banking has a duration mismatch though. Borrow short lend long is the business model, and generally it works fine. The issue here (imo) is the scale - the liquid part of their balance sheet that was supporting the short term deposits shouldn't have been in 10 year paper. Having their equity in 10 year paper (or even 30 year loans) isn't an issue, but having demand deposits backing long duration assets is an issue, especially given the lack of stickiness in their deposit base. If they had sold a few $B in 5 year CDs when they bought those bonds this would probably also have worked out.

And thats duration management? Like its one thing for a retail investor last January to think Ive got this bond index, and its cheap so Im good, not realizing the duration was something like 8.1 or whatever. And frankly, probably not understanding what that means in the first place. Thats not acceptable for a bank and surely not for the 16th largest bank in the US!

I get that they werent just holding a bond index, but its the same effect.

And thats duration management? Like its one thing for a retail investor last January to think Ive got this bond index, and its cheap so Im good, not realizing the duration was something like 8.1 or whatever. And frankly, probably not understanding what that means in the first place. Thats not acceptable for a bank and surely not for the 16th largest bank in the US!

I get that they werent just holding a bond index, but its the same effect.

Yeah, I think I agree with what you're saying in a slightly different way. Basically they need to have duration management, and obviously it was insufficient. But probably you wouldn't expect (or even want) perfect asset-liability duration matching in a bank, since that would really reduce net interest margins.

Average duration isn't a good proxy for that either - they'd actually have been better off with a 50/50 mix of tbills/30 year paper than an equivalent duration portfolio of 10-15 year bonds, because they wouldn't have needed to liquidate the long end of the portfolio in that situation, and could have covered withdrawals using the short end and kept the long end as held to maturity.

Obviously lots of ways to have avoided this on either the asset or liability side of the balance sheet, which is why its so egregious a failure for a pretty big institution.

The Following User Says Thank You to bizaro86 For This Useful Post:

Let's be clear, SVB did not collapse because of high interest rates and losing money on bonds. While that may have been the catalyst they collapsed because they had negative working capital and the perception that they were out of liquid cash (as they needed to raise funds to cover the loss on the fire sale of bonds). And with investors all looking to withdraw at the same time (a classic bank run), you have a bank who is unable to meet the demand suddenly collapsing. What bank has 42 billion sitting in cash available to make those payments? Without the bank run and hysteria, SVB would be standing today.

A bank run can occur at any bank, all that is needed is hysteria contagion to run amock. If the general population, which includes corporations, lose confidence in the banking system, fear will set in. Most American banks went down 10% on Thursday, solely due to hysteria.

We just have to look at the TP run craze in March 2020 to see what mass hysteria can do. All of a sudden toiler paper was a rare commodity because hysteria manifested an actual shortage, which further fed the hysteria in a vicious cycle. You can also look at the Argentine financial crisis of 2001 to see the damage of a bank run when you lose confidence in the system.

I personally believe, if the feds don't step in before Monday and make a statement to assure all investors and deposits that were held by SBV that they will be made whole, this uncertainty could certainly spread unchecked.

Too big to fail most certainly holds true here.

Last edited by Firebot; 03-11-2023 at 05:50 PM.

The Following User Says Thank You to Firebot For This Useful Post:

^really, that’s why a bank run is so dangerous. They’re all technically insolvent and if everyone demands their money all at once, it’s impossible for them.

I would argue that Silicon Valley Bank isn't just like any other bank because they catered to relatively few customers (compared to other banks their size) who had large deposits. Look at how small a percentage of their deposits were insured compared to other banks:

Spoiler!

That makes a run on it much more likely, and is also why they should have been more conservative in maintaining liquidity.

And while maintaining confidence in the banking sector is important, it's also not the government's job to protect a bank and venture capitalists from the fallout of their own terrible and risky decisions. The federal government lifted regulations at the behest of banks like this, and now taxpayers are supposed to pay for their mismanagement by funding the uninsured deposits?

Luckily in this case, it doesn't seem like the bank is anywhere near insolvent, they just won't be able to come up with the funds until they sell off their T-Bills. But depositors should get the vast majority of their funds back eventually.

I strongly disagree that SVB should be judged to big to fail. The criteria for that are laid out in advance and they don't qualify. It comes with real costs to those banks in terms of tighter regulations, so letting smaller banks like SVB off the hook for stress tests and then bailing them out anyway is a bad precedent.

Roku et all will get their money back eventually, they'll just have to wait for an orderly liquidation.

Where the fed should step in is if it becomes a contagion/crisis of confidence system wide. If it starts to spread THEN have the Fed guarantee all deposits for awhile to stabilize the system.

But the moral hazard of bailing out SVB now shouldn't happen. Anyone putting more than $250k into a bank should know the risks. Maybe bump it to $1MM per bank or something.

Janet Yellen says theyre not going to bail out SVB.

I don't think that was ever really in question. The bank is clearly going to fail. The question will be if they do anything for depositors.

It would set a pretty terrible precedent if they covered all the uninsured deposits; there'd be no point in FDIC limits (or private sector banking for that matter) if the government is just on the hook for it all when it goes wrong.

But I do think there is room for support in terms of liquidity. Something like government-funded bridge loans for affected depositors would probably make sense. So if the government estimates that uninsured account holders will eventually get 90 cents on the dollar, they could loan depositors up to say, 60-70% of their account value so they can make payroll and continue to operate. Then the government would get paid back when SVB's holdings are liquidated.

Yeah, I think those types of proposals have been batted around. The bank has failed and it’s a question of whether they do anything for depositors over and above the $250k. It’s a tough spot, really. On one hand you don’t want to encourage the moral risk, and on the other you don’t want contagion.

I think that contagion is obviously a huge risk, and it’s also quickly solved by backing the deposits. It’s going to be an interesting day and the open tomorrow will be as a result.