06-15-2012, 01:02 PM

06-15-2012, 01:02 PM

|

#41

|

|

Lifetime Suspension

|

Quote:

Originally Posted by hulkrogan

a 2 year for 3.9% or less?

Yes, I absolutely think that same offer will be there. Unless they are actually adding 5 years on, making this 8 more years at 3.9%. I'd still take that bet.

I don't think there are many ways you could financially handle this worse than signing a 5 year extension at 3.9%. I can't predict rates, so we'll have to wait 3 years and see, but give me a time in history, and I'll show you that this would have been a bad choice, every time.

|

This is what he said "I am two years into a 5 year fixed at 3.9%. My lender has offered to renew for another 5 years at the same rate of 3.9%. No fees or anything. "

I'm sure you'll pay RubberDuck's mortage if rates get jacked eh?

I honestly don't think arguing about half a percent is being "bent over" for the piece of mind a locked in low rate brings.

Your right you can't predict rates, and I would never ask your advice

Why don't you ask the people who had mortages in the 80's "every time"

|

|

|

|

06-15-2012, 01:05 PM

|

#42

|

|

Ate 100 Treadmills

|

Quote:

Originally Posted by ranchlandsselling

3.90% for three years blended with 3.29% (likely the best his bank is offering) for two years with the penalty blended into the rate is less than the 3.90% they're offering you. They're charging you the penatly either way. It's just blended into the rate.

Do the math on what your payments would be at current rates plus the penalty vs. your current mortgage vs. what they're offering you and see which one works out best. I don't have time to get into this more but feel free to PM me.

|

That's a pretty good calculation there considering you have no idea what the actual interest owing is and the principle of the remaining mortgage.

Under some circumstances he will save by simply breaking the morgage. Depends on the rate he can get and how much is left on the mortgate.

My girlfrien's parents were paying 3.9% with 2 years left. They had 400k left on the mortgage, and were able to get a 2.99% fixed 5 year. I advised them to pay the penalty and pay the fee, as in this case it was a no brainer.

Whether or not you should pay the penalty should be based on a calculation dependent on your specific situation.

|

|

|

|

|

06-15-2012, 01:08 PM

|

#43

|

|

Playboy Mansion Poolboy

Join Date: Apr 2004

Location: Close enough to make a beer run during a TV timeout

|

Quote:

Originally Posted by hulkrogan

but give me a time in history, and I'll show you that this would have been a bad choice, every time.

|

Late 1970s?

I agree with what you are saying; that in the past several years the rates have been going down. And if they don't continue down, we likely won't see 1980s rates again.

That being said; if somebody in 1978 had signed a 10 year deal for 8.99%- he would have been the one laughing in the early 80s.

|

|

|

|

|

06-15-2012, 01:31 PM

|

#44

|

|

My face is a bum!

|

Quote:

Originally Posted by stacey

This is what he said "I am two years into a 5 year fixed at 3.9%. My lender has offered to renew for another 5 years at the same rate of 3.9%. No fees or anything. "

I'm sure you'll pay RubberDuck's mortage if rates get jacked eh?

I honestly don't think arguing about half a percent is being "bent over" for the piece of mind a locked in low rate brings.

Your right you can't predict rates, and I would never ask your advice

Why don't you ask the people who had mortages in the 80's "every time"

|

Stacey, you are bad at math.

A 3.9% for another 5 years is worse than breaking his current mortgage and signing a new 5 year fixed, so to suggest that is a good idea shows you should stop posting in this thread.

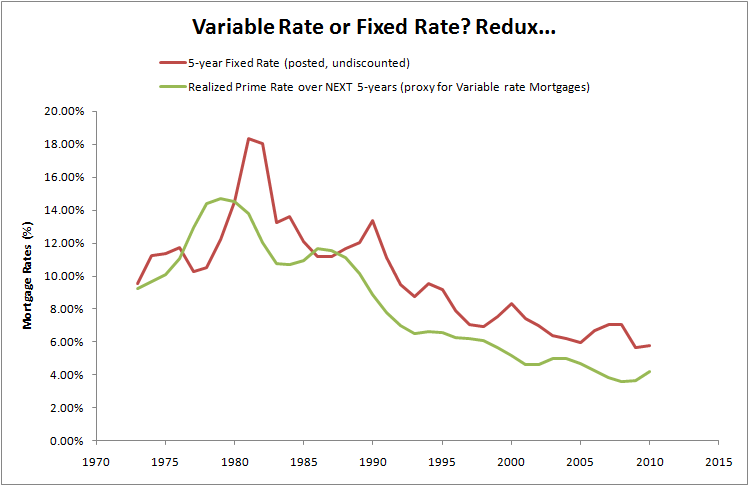

There has been one brief period where fixed has been better, and one very brief blip after that. If you were going on 5 year fixed mortgages during this you might have hit one of these times, but they were less than 5 year windows, so you might have hit none of them. Variable terms are cheaper 89% of the time in Canadian history. If you are going to go 5 year fixed over the life of your mortgage, if that is 4 terms or more (20 years or more to pay back the mortgage) there is not once in Canadian history where you would save money with the fixed.

So have fun spending $60,000+ on your "peace of mind" for that 11% chance.

|

|

|

|

|

06-15-2012, 02:04 PM

|

#45

|

|

Lifetime Suspension

|

Just leave it at "I can't predict rates"

Mr. "everytime"

|

|

|

|

|

06-15-2012, 02:33 PM

|

#46

|

|

My face is a bum!

|

Quote:

Originally Posted by stacey

Just leave it at "I can't predict rates"

Mr. "everytime"

|

You don't need to predict rates.

You need to understand the spread in interest rates and flexibility in fixed vs. variable mortgages.

Sorry you can't understand simple economics, luckily you have personal insults mastered at a remedial level.

I might be tempted to jump on a 5 year or less fixed right now if I was up for renewal as the spread between variable and fixed is quite narrow right now. But really, its just taking an 11% gamble and throwing in some educated guessing and hoping for the best.

Stacey, if you know interest rates are going to be above 3.9% in the coming future there are many investment strategies that will make you a millionaire. I'm guessing you don't know when rates are going to go up or down yourself, and haven't already made millions with your superior mortgage knowledge.

Last edited by Bill Bumface; 06-15-2012 at 02:40 PM.

|

|

|

|

|

06-15-2012, 02:40 PM

|

#47

|

|

Lifetime Suspension

|

Quote:

Originally Posted by hulkrogan

You don't need to predict rates.

You need to understand the spread in interest rates and flexibility in fixed vs. variable mortgages.

Sorry you can't understand simple economics, luckily you have personal insults mastered at a remedial level.

|

Right because rates are going to be 2.99 for the next 7-10 years right? That would be the only way your "logic" works and people are "bent" over with a 3.9% rate.

Your magical rate world is due for a shake up...

|

|

|

|

|

06-15-2012, 02:48 PM

|

#48

|

|

Playboy Mansion Poolboy

Join Date: Apr 2004

Location: Close enough to make a beer run during a TV timeout

|

Quote:

Originally Posted by hulkrogan

Stacey, you are bad at math.

,snip.

So have fun spending $60,000+ on your "peace of mind" for that 11% chance.

|

Just curious how you came up with that costing $60K. Over a 5 year term the difference between borrowing $400K at 2.99% and 3.9% seems to be about $12,000.

|

|

|

|

|

06-15-2012, 02:51 PM

|

#49

|

|

Ate 100 Treadmills

|

Quote:

Originally Posted by hulkrogan

Stacey, you are bad at math.

A 3.9% for another 5 years is worse than breaking his current mortgage and signing a new 5 year fixed, so to suggest that is a good idea shows you should stop posting in this thread.

There has been one brief period where fixed has been better, and one very brief blip after that. If you were going on 5 year fixed mortgages during this you might have hit one of these times, but they were less than 5 year windows, so you might have hit none of them. Variable terms are cheaper 89% of the time in Canadian history. If you are going to go 5 year fixed over the life of your mortgage, if that is 4 terms or more (20 years or more to pay back the mortgage) there is not once in Canadian history where you would save money with the fixed.

So have fun spending $60,000+ on your "peace of mind" for that 11% chance.

|

Basically, you argument breaks down into rates have been falling for the last 30 years (except for when they went up), so we should bank on that and always get a variable rate.

When rates are rising, fixed is better. I know there has only been one period in the last 35 years where that has happened, but now rates are at an all time low and really have nowhere to go but up.

The thing is, that the spread between variable and fixed rates is quite significant right now, as banks are accomodating for the fact rates will go up. The people at the banks setting the rates are a lot more knowledgable than anyone here. So at any given time, it should, in theory, be a coin flip between variable and fixed. Except when banks are in a pricing war and offering 2.99% fixed...then I'd definitely go fixed.

|

|

|

|

|

06-15-2012, 03:33 PM

|

#50

|

|

My face is a bum!

|

Quote:

Originally Posted by blankall

Basically, you argument breaks down into rates have been falling for the last 30 years (except for when they went up), so we should bank on that and always get a variable rate.

When rates are rising, fixed is better. I know there has only been one period in the last 35 years where that has happened, but now rates are at an all time low and really have nowhere to go but up.

The thing is, that the spread between variable and fixed rates is quite significant right now, as banks are accomodating for the fact rates will go up. The people at the banks setting the rates are a lot more knowledgable than anyone here. So at any given time, it should, in theory, be a coin flip between variable and fixed. Except when banks are in a pricing war and offering 2.99% fixed...then I'd definitely go fixed.

|

Yup, on a big up-kick you can definitely beat variable on a fixed. The problem is, how do you know when that up-kick is coming? I was told by everyone and everything I read that rates where going up when I signed on 3 years ago for a 5 year 3.65. That was the historical low for 5 year fixed rates ever, and everyone, including the BOC was warning that rates were going up in a matter of months. I couldn't lose! Oops.

Now maybe the fact I'm locked in a 5 year means I'll miss that big up-kick, and my next 5 year (in 2 years) will suck. See how easy it is to lose?

I can totally understand taking a gamble on a 2.99 right now. It looks like not a bad idea at all. But 3.9 does not look good at all.

Fixed rates are determined by the bond market, not "the bank". The fact you can get a 10 year 3.89 right now suggests the market is banking on interest rates being below that level for the next 10 years.

As soon as interest rates show a sniff of skyrocketing, bond yields will go through the roof, and the spread between variable and fixed will make you cry, and it's too late to do anything about it.

An increasing interest rate environment doesn't mean that fixed is better. An unexpected increasing interest rate environment does.

|

|

|

|

|

06-15-2012, 03:45 PM

|

#51

|

|

Lifetime Suspension

|

LOl... "take a gamble on 2.99"

I guess we'll just have to wait and see Nostradamus....

|

|

|

|

|

06-15-2012, 03:57 PM

|

#52

|

|

My face is a bum!

|

Quote:

Originally Posted by stacey

LOl... "take a gamble on 2.99"

I guess we'll just have to wait and see Nostradamus....

|

You are the worst. Why do I waste my time using economics and math refuting your posts?? ..... Chris Angel!!

|

|

|

|

|

The Following User Says Thank You to Bill Bumface For This Useful Post:

|

|

|

06-15-2012, 04:12 PM

|

#53

|

|

Ate 100 Treadmills

|

Quote:

Originally Posted by hulkrogan

Yup, on a big up-kick you can definitely beat variable on a fixed. The problem is, how do you know when that up-kick is coming? I was told by everyone and everything I read that rates where going up when I signed on 3 years ago for a 5 year 3.65. That was the historical low for 5 year fixed rates ever, and everyone, including the BOC was warning that rates were going up in a matter of months. I couldn't lose! Oops.

Now maybe the fact I'm locked in a 5 year means I'll miss that big up-kick, and my next 5 year (in 2 years) will suck. See how easy it is to lose?

I can totally understand taking a gamble on a 2.99 right now. It looks like not a bad idea at all. But 3.9 does not look good at all.

Fixed rates are determined by the bond market, not "the bank". The fact you can get a 10 year 3.89 right now suggests the market is banking on interest rates being below that level for the next 10 years.

As soon as interest rates show a sniff of skyrocketing, bond yields will go through the roof, and the spread between variable and fixed will make you cry, and it's too late to do anything about it.

An increasing interest rate environment doesn't mean that fixed is better. An unexpected increasing interest rate environment does.

|

I think the problem with your analysis that I'm having is that you are relying too much on what's happened in the past. You are using the fact that interest rates stayed low for longer than expected this time to suggest that trend will happen in the future.

Don't get me wrong, I agree with you, in many situations, a variable is better. I have a variable myself. I got it about 14 months ago. At that point fixed was at 3.6, variable was prime -.9% (effective rate of 2.1%), and the general consensus was rates would stay low for another year.

Now with variable at prime -.6%, fixed at around 3%, and much more uncertainty in as to interest rates in the future, I'd go fixed right now. Compared to a year ago, there's more uncertainty with rates, and the spread between fixed and variable is much smaller.

|

|

|

|

|

06-15-2012, 04:39 PM

|

#54

|

|

My face is a bum!

|

Quote:

Originally Posted by blankall

I think the problem with your analysis that I'm having is that you are relying too much on what's happened in the past. You are using the fact that interest rates stayed low for longer than expected this time to suggest that trend will happen in the future.

Don't get me wrong, I agree with you, in many situations, a variable is better. I have a variable myself. I got it about 14 months ago. At that point fixed was at 3.6, variable was prime -.9% (effective rate of 2.1%), and the general consensus was rates would stay low for another year.

Now with variable at prime -.6%, fixed at around 3%, and much more uncertainty in as to interest rates in the future, I'd go fixed right now. Compared to a year ago, there's more uncertainty with rates, and the spread between fixed and variable is much smaller.

|

Really all anyone, including the bond market, has to go on is the past.

I'm not going to argue at all that right now might be one of the times to go fixed. As you say, the spread is really tight between fixed and variable, and interest rates dropping seems like a slim to none possibility at the moment. The downside of getting it wrong right now is quite small, as you say -.6%. The possible upside is a lot more than that. If I was up for renewal right now I'd very seriously consider a 2.99.

I still think 3.9 for 5 years is ######ed...

|

|

|

|

|

06-15-2012, 04:43 PM

|

#55

|

|

Ate 100 Treadmills

|

Quote:

Originally Posted by hulkrogan

Really all anyone, including the bond market, has to go on is the past.

I'm not going to argue at all that right now might be one of the times to go fixed. As you say, the spread is really tight between fixed and variable, and interest rates dropping seems like a slim to none possibility at the moment. The downside of getting it wrong right now is quite small, as you say -.6%. The possible upside is a lot more than that. If I was up for renewal right now I'd very seriously consider a 2.99.

I still think 3.9 for 5 years is ######ed...

|

Well like I said before, it all depends on the math, which is individual to each situation. For some it makes sense to break and pay the penalty, for others the extension for an additional 2 years might make sense.

I agree 3.9% is ######ed, but we aren't talking about simply just taking a 3.9% rate. We're talking about potentially breaking an existing agreement, which will go on for 3 years.

|

|

|

|

|

06-15-2012, 05:12 PM

|

#56

|

|

My face is a bum!

|

Quote:

Originally Posted by blankall

Well like I said before, it all depends on the math, which is individual to each situation. For some it makes sense to break and pay the penalty, for others the extension for an additional 2 years might make sense.

I agree 3.9% is ######ed, but we aren't talking about simply just taking a 3.9% rate. We're talking about potentially breaking an existing agreement, which will go on for 3 years.

|

Yup, breaking a 3.9, paying the penalty, and dropping to a 2.99 is a different can of worms, and a bit of a guessing game.

|

|

|

|

|

06-15-2012, 05:21 PM

|

#57

|

|

Franchise Player

|

Where can you get a variable rate with P-0.6%?

|

|

|

|

|

06-15-2012, 05:26 PM

|

#58

|

|

Ate 100 Treadmills

|

Quote:

Originally Posted by albertGQ

Where can you get a variable rate with P-0.6%?

|

Just play the banks off eachother. Go to your bank ask them their rate. Find another bank, ask if they can beat it. Go back and forth until you find the rate you want. Usually the bank you are already with for a long time will give it to you.

I managed to get P-0.9% but this was about 14 months ago. I don't think my bank (CIBC) would go that low anymore.

|

|

|

|

|

06-15-2012, 08:54 PM

|

#59

|

|

Franchise Player

|

I thought you said you can get P-0.6% now. The best I've seen is P-0.1%

|

|

|

|

|

06-16-2012, 09:43 AM

|

#60

|

|

Powerplay Quarterback

|

Quote:

Originally Posted by blankall

That's a pretty good calculation there considering you have no idea what the actual interest owing is and the principle of the remaining mortgage.

Under some circumstances he will save by simply breaking the morgage. Depends on the rate he can get and how much is left on the mortgate.

My girlfrien's parents were paying 3.9% with 2 years left. They had 400k left on the mortgage, and were able to get a 2.99% fixed 5 year. I advised them to pay the penalty and pay the fee, as in this case it was a no brainer.

Whether or not you should pay the penalty should be based on a calculation dependent on your specific situation.

|

It's pretty easy to figure out.

The bank takes your current rate and charges you an IRD penalty based on their best rate of their choice. They'll then figure out what they need to mark up their "current" rate to make it even. They'll then give you that rate for 5 years instead of your current rate for (I think he said 3) more years essentially selling you on the two extra years at low rates. Problem is that if you're sitting down with your bank your likely not getting a best current rate. So you're screwed from the get go. You're paying a penalty to break your mortgage (even though your bank seems to tell you you're not, they'll sell you on blend and extend and a blended rate. The rate is blended, but so is your penalty ontop of that via a higher rate. You're paying them one way or another. It's just if after all that you then go and get the best rate or a poorer rate they're offering you.

I love the condescension, blathering away about making comments without even knowing the current actual interest owing, principal, when you follow up with this gem

Quote:

|

Originally Posted by blankall

The issue is that he is already locked in for 3 more years. He can't get the 2.99 rate or the 10 year deal without paying about $6000 to break his current mortgage.

|

Not to mention you then follow up with a comment about your girlfriends parents and how you heroically suggested they do the EXACT same thing most of us suggested the guy asking the questions should consider.

Finally I then wrapped up my comments suggesting the poster do the math on the three scenarios to figure out which one works best and even offered to help.

Not once did the poster ask about variable rates which are a completely different discussion. Some people simply don't like the worrying about rates.

The variable rate debate is in favour of variable until it's not. Pretty poor answer but at some point the history of variable beating fixed 99% of the time will result in the 1% happening. I'd wager the chance of that 1% right now is a lot higher than ever in the past. You could still very easily win out on variable over fixed right now. But I'm less comfortable betting on in now that I would have been 2 years ago.

Then there's stacey, WTF is he talking about.

Poster asked about locking a rate at 3.90%, for 5 years (so 2012 - 2017) hulk suggests consider getting 2.99% for five years (so 2012 - 2017) and paying the penalty and stacey goes off that 3.90% is a great rate to get for 5 years, 2.99% isn't going to last forever (which is totally irrelevant), you can't predict rates mr HulkRogan "just leave it at "I can't predict rates"" and the poster should take the 3.90% because of. . . . Chat to those people from the 80's??

How does that even make sense?

Was yesterday afternoon a full moon or something ??

What's with people just being jerks?

Last edited by ranchlandsselling; 06-16-2012 at 10:05 AM.

|

|

|

|

Posting Rules

Posting Rules

|

You may not post new threads

You may not post replies

You may not post attachments

You may not edit your posts

HTML code is Off

|

|

|

All times are GMT -6. The time now is 05:59 AM.

|

|