04-10-2023, 01:31 PM

04-10-2023, 01:31 PM

|

#1181

|

|

Franchise Player

Join Date: Mar 2002

Location: Auckland, NZ

|

Quote:

Originally Posted by Table 5

I would do the dance of joy if my condo broke even this decade.

|

Me too! It's been going on 15 years now...

|

|

|

|

04-10-2023, 01:54 PM

|

#1182

|

|

First Line Centre

|

Quote:

Originally Posted by Mr.Coffee

Will there be a correction in automobile pricing though?

I tend to think there might be.

|

Manufacturers have changed their tune since COVID and are now willingly cutting production to optimize inventories and limiting the need for dealers to discount from MSRP.

Even with reduced demand do to economic concerns and affordability issues due to higher finance rates, I can imagine a scenario where production is also cut to keep used car prices up; afterall, the majority of new cars are financed through the manufacturers, and they have an interest in not crashing the used market.

I'm not saying things will stay as frothy as they've been, but there are a number of mechanisms in place to prevent a market crash like some are predicting...

|

|

|

|

04-10-2023, 02:13 PM

|

#1183

|

|

Franchise Player

Join Date: Jun 2004

Location: Calgary

|

Quote:

Originally Posted by Slava

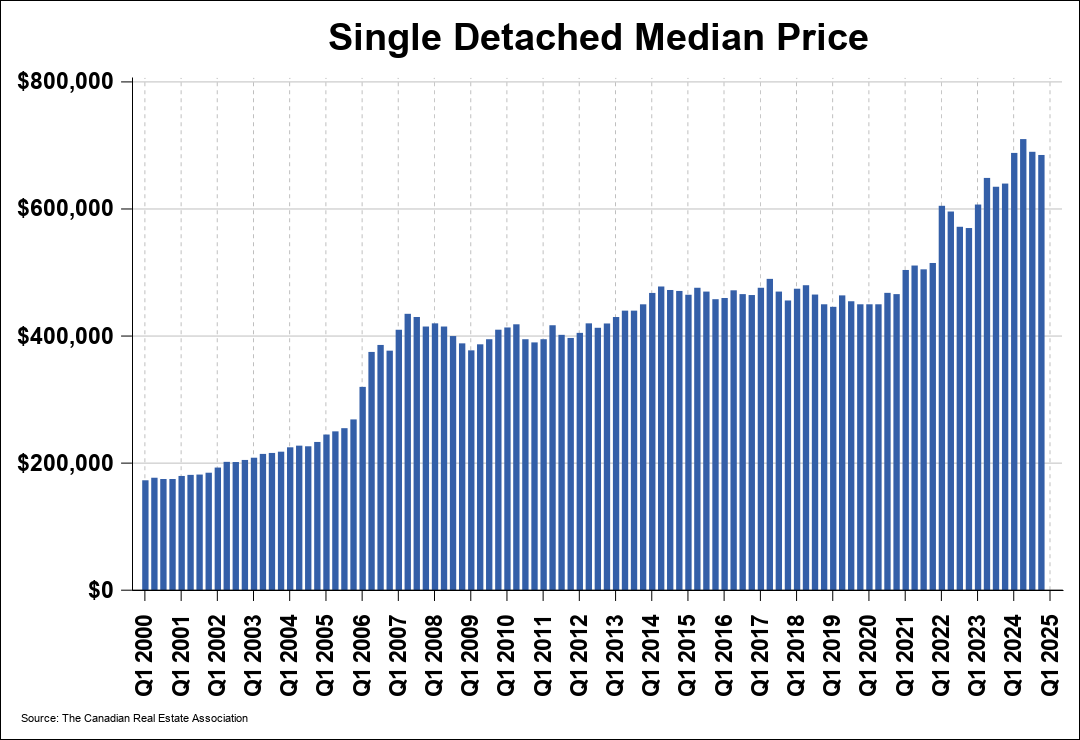

Well have a look at this graph. It's been up the last year or so, but outside of that, there's been almost nothing by and large for years.

|

No, between 2007 and 2020 it was growing at a reasonable rate roughly matching inflation. It was bonkers both before and after that.

Based on the CPI a 410k house in 2007 should be worth 510k in 2020, which roughly matches your graph.

The real estate market is not the stock market, as a society we should not be expecting or wanting 10% annual returns. The only thing that does is enrich the older generations at the expense of future ones while providing no value.

|

|

|

|

|

04-10-2023, 02:40 PM

|

#1184

|

|

damn onions

|

Quote:

Originally Posted by you&me

Manufacturers have changed their tune since COVID and are now willingly cutting production to optimize inventories and limiting the need for dealers to discount from MSRP.

Even with reduced demand do to economic concerns and affordability issues due to higher finance rates, I can imagine a scenario where production is also cut to keep used car prices up; afterall, the majority of new cars are financed through the manufacturers, and they have an interest in not crashing the used market.

I'm not saying things will stay as frothy as they've been, but there are a number of mechanisms in place to prevent a market crash like some are predicting...

|

Do you sell cars?

|

|

|

|

|

04-10-2023, 02:54 PM

|

#1185

|

|

First Line Centre

Join Date: Feb 2010

Location: Mckenzie Towne

|

While predicting future rates is impossible, and something I try to avoid, I have a program that can determine what an interest rate at renewal on a 3-year fixed (for example) would need to be in order for it to out-perform taking a lower 5-year fixed rate. So it essentially spits out a number where "if rates are at ____% or lower at renewal, then you're best bet is to take the shorter term".

This allows you to at least see what rates would need to be at in the future, then determine how feasible that is.

If anyone is coming up for renewal and is deciding between these two options, PM me and I can run #s for you.

|

|

|

|

|

The Following 3 Users Say Thank You to MillerTime GFG For This Useful Post:

|

|

|

04-10-2023, 03:04 PM

|

#1186

|

|

Franchise Player

Join Date: Dec 2006

Location: Calgary, Alberta

|

Quote:

Originally Posted by Dan02

No, between 2007 and 2020 it was growing at a reasonable rate roughly matching inflation. It was bonkers both before and after that.

Based on the CPI a 410k house in 2007 should be worth 510k in 2020, which roughly matches your graph.

The real estate market is not the stock market, as a society we should not be expecting or wanting 10% annual returns. The only thing that does is enrich the older generations at the expense of future ones while providing no value.

|

Yeah, going from memory, I think the long term growth in real estate is about 4.1%/yr. I dont think it should be double digit growth every year. At the same time though, that 4.1% average is lumpy. It mean mean a year at zero and a year at 8.2% and that sort of thing. Its cyclical and in Calgary that also coincides with the energy market as a significant driver. I think were both basically on the same page here?

|

|

|

|

|

04-10-2023, 04:53 PM

|

#1187

|

|

Appealing my suspension

Join Date: Sep 2002

Location: Just outside Enemy Lines

|

Quote:

Originally Posted by MillerTime GFG

While predicting future rates is impossible, and something I try to avoid, I have a program that can determine what an interest rate at renewal on a 3-year fixed (for example) would need to be in order for it to out-perform taking a lower 5-year fixed rate. So it essentially spits out a number where "if rates are at ____% or lower at renewal, then you're best bet is to take the shorter term".

This allows you to at least see what rates would need to be at in the future, then determine how feasible that is.

If anyone is coming up for renewal and is deciding between these two options, PM me and I can run #s for you.

|

I don't have a spreadsheet set up for this, but I do a lot of scenarios in the free calculators you can get on the web. Just that rates increased in less than half the time frame I expected and ballooned about 1.5% above what I anticipated as the peak. One day my feeble brain will learn to account for how extreme today's markets are.

__________________

"Some guys like old balls"

Patriots QB Tom Brady

|

|

|

|

|

The Following User Says Thank You to Sylvanfan For This Useful Post:

|

|

|

04-10-2023, 09:16 PM

|

#1188

|

|

Franchise Player

|

Quote:

Originally Posted by Dan02

No, between 2007 and 2020 it was growing at a reasonable rate roughly matching inflation. It was bonkers both before and after that.

Based on the CPI a 410k house in 2007 should be worth 510k in 2020, which roughly matches your graph.

The real estate market is not the stock market, as a society we should not be expecting or wanting 10% annual returns. The only thing that does is enrich the older generations at the expense of future ones while providing no value.

|

I think in Calgary you need to differentiate between SFH and condo/THs as they two stories are opposite.

|

|

|

|

|

04-11-2023, 05:41 AM

|

#1189

|

|

Franchise Player

Join Date: Jun 2004

Location: Calgary

|

Quote:

Originally Posted by GGG

I think in Calgary you need to differentiate between SFH and condo/THs as they two stories are opposite.

|

No not really, to Slavas point, it was just more lumpy. If your timing was terrible then yes you might feel that way despite the data not supporting it. Full disclosure I got sucked into the mania in 2007-8 and bought in at the peak as well. I was basically down/flat in value for 13 years before spiking the last couple of years.

From the CREA data set, in Q1 2000 the average apartment sale price was around 115,000, matching inflation values it should now be around 190,000 today, however it's now around 250,000.

If you agree with my postulate that for the betterment of society we should preserve the ability of future generations to be able to afford housing, then to return to the 2000 levels of affordability we'd need another 15 years of zero appreciation in the price of apartments coupled with 2% inflation to match the 2000 affordability levels.

The idea that housing is an investment that should appreciate needs to be broken and reversed. Why because any value higher then inflation over the long run ends up with housing being impossibly unaffordable.

Even Slavas 4.1% number vs a 2% inflation means every single generation(20 years) housing is 50% more expensive in real dollars then the previous generation. Something eventually has to break and the longer it goes without breaking the worse it will be when it does.

|

|

|

|

|

04-11-2023, 06:09 PM

|

#1190

|

|

Ate 100 Treadmills

|

Quote:

Originally Posted by Dan02

No not really, to Slavas point, it was just more lumpy. If your timing was terrible then yes you might feel that way despite the data not supporting it. Full disclosure I got sucked into the mania in 2007-8 and bought in at the peak as well. I was basically down/flat in value for 13 years before spiking the last couple of years.

From the CREA data set, in Q1 2000 the average apartment sale price was around 115,000, matching inflation values it should now be around 190,000 today, however it's now around 250,000.

If you agree with my postulate that for the betterment of society we should preserve the ability of future generations to be able to afford housing, then to return to the 2000 levels of affordability we'd need another 15 years of zero appreciation in the price of apartments coupled with 2% inflation to match the 2000 affordability levels.

The idea that housing is an investment that should appreciate needs to be broken and reversed. Why because any value higher then inflation over the long run ends up with housing being impossibly unaffordable.

Even Slavas 4.1% number vs a 2% inflation means every single generation(20 years) housing is 50% more expensive in real dollars then the previous generation. Something eventually has to break and the longer it goes without breaking the worse it will be when it does.

|

A few points:

1. We might be seeing 30+% inflation, total over the last few years. This is going to offset a large portion of the nominal increase in value. Of course fixed wage earners aren't going to benefit from this.

2. With a quickly growing population and the land supply remaining more or less flat, we are likely seeing a quick decrease in the quality of housing available to future generations.

Providing future generations with housing of the same quality and price simply is not possible with the current conditions.

Housing will continue to be seen as a good investment as long as their is a shortage of supply.

|

|

|

|

|

04-11-2023, 07:15 PM

|

#1191

|

|

Franchise Player

|

Quote:

Originally Posted by blankall

2. With a quickly growing population and the land supply remaining more or less flat, we are likely seeing a quick decrease in the quality of housing available to future generations.

|

Canada has room for hundreds of millions more people even at reasonable population densities only in the southern populated parts of the country.

If you're talking about a supply of zoned land that's true, but making a bad political decision to limit residential use of land isn't the same thing as having a shortage of land.

|

|

|

|

|

The Following User Says Thank You to bizaro86 For This Useful Post:

|

|

|

04-11-2023, 08:24 PM

|

#1192

|

|

Ate 100 Treadmills

|

Quote:

Originally Posted by bizaro86

Canada has room for hundreds of millions more people even at reasonable population densities only in the southern populated parts of the country.

If you're talking about a supply of zoned land that's true, but making a bad political decision to limit residential use of land isn't the same thing as having a shortage of land.

|

Don't disagree at all. Canada clearly has the land. They aren't letting people use it though.

|

|

|

|

|

04-12-2023, 09:19 AM

|

#1194

|

|

Franchise Player

|

Big jobs numbers.

https://www.theglobeandmail.com/busi...th-march-2023/

Another Canadian jobs report has come out. Another set of employment numbers has defied expectations. Another month of rock-solid employment growth is in the books.

And economists despair.

What a strange place, this postpandemic world.

Last Thursdays labour force survey from Statistics Canada showed that employment rose by another 35,000 jobs in March, defying forecasters expectations that the labour market would at least take a breather after adding a ridiculous 172,000 jobs in the first two months of the year. It marked the seventh consecutive month of growth, during which the economy has added nearly 400,000 jobs.

|

|

|

|

|

04-12-2023, 09:22 AM

|

#1195

|

|

Crash and Bang Winger

|

I just renewed for 3 year at 4.79% after my 5 year fixed at 3.39% expired. Missed the entire low COVID rate period. Do I kick myself for not going variable 5 years ago, during COVID I sure did, last year+ no. Hindsight is 20/20.

I know Variable beats Fixed "always" long term, but to know exactly what my payment is every month and being comfortable with it saves me the mental stress which is worth the "premium" of being fixed.

Do what is right for you, none of us know what the correct answer is.

Also, if you have cash laying around and don't think you can beat 5% (after tax) in the markets, use it to pay down your mortgage as that is like getting a 5% return on your capital.

|

|

|

|

|

The Following 6 Users Say Thank You to Qwerty For This Useful Post:

|

|

|

04-12-2023, 10:16 AM

|

#1196

|

|

Ate 100 Treadmills

|

Quote:

Originally Posted by Qwerty

I just renewed for 3 year at 4.79% after my 5 year fixed at 3.39% expired. Missed the entire low COVID rate period. Do I kick myself for not going variable 5 years ago, during COVID I sure did, last year+ no. Hindsight is 20/20.

I know Variable beats Fixed "always" long term, but to know exactly what my payment is every month and being comfortable with it saves me the mental stress which is worth the "premium" of being fixed.

Do what is right for you, none of us know what the correct answer is.

Also, if you have cash laying around and don't think you can beat 5% (after tax) in the markets, use it to pay down your mortgage as that is like getting a 5% return on your capital.

|

3 years fixed at 4.79% is a pretty solid decision IMO. You're only paying 1.4% more than you were, and should hopefully be in a position to get a lower rate in 3 years.

From what I've seen most banks are offering much better rates for a 5 year term than a 3 year term, as they want to get people locked in at a high rate for a longer term. You were able to negotiate a solid rate for a three year term.

As for variable vs. fixed, variable rates are currently at about 1.25-1.5% higher than fixed ones. So in your case, with a 3 year mortgage, you'd need to see some pretty quick drops (like 1.5% in the next 1.5 years or so) to not come out at about the same with fixed.

|

|

|

|

|

The Following User Says Thank You to blankall For This Useful Post:

|

|

|

04-12-2023, 11:17 AM

|

#1197

|

|

Appealing my suspension

Join Date: Sep 2002

Location: Just outside Enemy Lines

|

They held the rates today although I suspect they would have preferred to increase.

I was offered a 5 year fixed at 4.19 today which is tempting. Let's me move from my Variable that is 6.25 to that three months early. But the penalty is rate differential. I expect rates will come down eventually, but I can't see them getting back down to that 3.5 range in the next 5 years.

__________________

"Some guys like old balls"

Patriots QB Tom Brady

|

|

|

|

|

04-12-2023, 11:29 AM

|

#1198

|

|

Powerplay Quarterback

|

Quote:

Originally Posted by Sylvanfan

They held the rates today although I suspect they would have preferred to increase.

I was offered a 5 year fixed at 4.19 today which is tempting. Let's me move from my Variable that is 6.25 to that three months early. But the penalty is rate differential. I expect rates will come down eventually, but I can't see them getting back down to that 3.5 range in the next 5 years.

|

Most the main bank's curves would have to be projecting year 4 and 5 below the 3.5% range to get to a 4.2% 5 year fixed.

|

|

|

|

|

The Following User Says Thank You to Leondros For This Useful Post:

|

|

|

04-12-2023, 11:51 AM

|

#1199

|

|

damn onions

|

Quote:

Originally Posted by Qwerty

I just renewed for 3 year at 4.79% after my 5 year fixed at 3.39% expired. Missed the entire low COVID rate period. Do I kick myself for not going variable 5 years ago, during COVID I sure did, last year+ no. Hindsight is 20/20.

I know Variable beats Fixed "always" long term, but to know exactly what my payment is every month and being comfortable with it saves me the mental stress which is worth the "premium" of being fixed.

Do what is right for you, none of us know what the correct answer is.

Also, if you have cash laying around and don't think you can beat 5% (after tax) in the markets, use it to pay down your mortgage as that is like getting a 5% return on your capital.

|

And a very critical point- its a riskless 5% return.

Pretty good if you ask me.

|

|

|

|

|

The Following 3 Users Say Thank You to Mr.Coffee For This Useful Post:

|

|

|

04-12-2023, 11:52 AM

|

#1200

|

|

Franchise Player

|

Quote:

Originally Posted by Leondros

Most the main bank's curves would have to be projecting year 4 and 5 below the 3.5% range to get to a 4.2% 5 year fixed.

|

Mortgage rates are based on the current five year yield, not based on a banks internal expectations for future interest rates. They do an asset/liability match and lock in the spread over the mortgage period.

So a five year mortgage will be mostly funded with 5 year money of some sort (Canada mortgage bonds, bank 5 year debt, 5 year GICs, etc).

The current 5 year GoC rate is down to 3% from its recent peak. It got over 3.8% in October, so fixed mortgage rates have followed it down somewhat.

Longer mortgage rates are lower than shorter mortgage rates right now because the yield curve is inverted.

|

|

|

|

Posting Rules

Posting Rules

|

You may not post new threads

You may not post replies

You may not post attachments

You may not edit your posts

HTML code is Off

|

|

|

All times are GMT -6. The time now is 10:37 AM.

|

|