02-01-2012, 12:34 PM

02-01-2012, 12:34 PM

|

#2021

|

|

Powerplay Quarterback

|

Quote:

Originally Posted by Red

I believe I did. Your question is quite irrelevant.

|

You didn't.

You accused a CMHC mortgage of being a taxpayer subsidized item when it's not nor has one ever been.

You then replied to that with a rhetoric question.

I'll move on to other conversations now.

|

|

|

|

02-01-2012, 12:38 PM

|

#2022

|

|

Lifetime Suspension

|

Quote:

Originally Posted by ranchlandsselling

You didn't.

You accused a CMHC mortgage of being a taxpayer subsidized item when it's not nor has one ever been.

You then replied to that with a rhetoric question.

I'll move on to other conversations now.

|

You are confused. Someone else did that.

|

|

|

|

|

02-01-2012, 12:49 PM

|

#2023

|

|

Franchise Player

Join Date: Feb 2006

Location: Toledo OH

|

Quote:

Originally Posted by ranchlandsselling

You didn't.

You accused a CMHC mortgage of being a taxpayer subsidized item when it's not nor has one ever been.

You then replied to that with a rhetoric question.

I'll move on to other conversations now.

|

The risk is underwritten by the taxpayer. Ultimately they will be on the hook if the real estate market declines. What enables a person to buy a home with 20 to 1 leverage in this country is ultimately the assumption of that risk that a crown corporation takes on. It's a risk that the banks by themselves won't make on a large scale (Which should not be easily dismissed).

Take your provided Q2 numbers on CMHC. With 9% of their loan protfolio being 90% or greater LTV then a national decline of 10% (much less than the 25% haircut the Americans took) puts roughly $50 billion of CMHC insured mortgages underwater. Now of course not all of those people are going to default, but the point stands that the CMHC's portfolio certainly has the potential to have to be bailed out.

|

|

|

|

|

02-01-2012, 01:19 PM

|

#2024

|

|

Powerplay Quarterback

|

Quote:

Originally Posted by Red

You are confused. Someone else did that.

|

Yup, I'm totally confused. Sorry about that. You replied so quickly to my post I thought it was a continuation of our coversation.

|

|

|

|

|

02-01-2012, 01:28 PM

|

#2025

|

|

Lifetime Suspension

|

Quote:

Originally Posted by ranchlandsselling

Yup, I'm totally confused. Sorry about that. You replied so quickly to my post I thought it was a continuation of our coversation.

|

Too quick for ya. No disagreement there

|

|

|

|

|

02-01-2012, 02:29 PM

|

#2026

|

|

Powerplay Quarterback

|

Quote:

Originally Posted by Red

Too quick for ya. No disagreement there |

Bah - back to not continuing the conversation with you!

|

|

|

|

|

02-01-2012, 05:24 PM

|

#2027

|

|

Powerplay Quarterback

|

Quote:

Originally Posted by Cowboy89

The risk is underwritten by the taxpayer. Ultimately they will be on the hook if the real estate market declines. What enables a person to buy a home with 20 to 1 leverage in this country is ultimately the assumption of that risk that a crown corporation takes on. It's a risk that the banks by themselves won't make on a large scale (Which should not be easily dismissed).

Take your provided Q2 numbers on CMHC. With 9% of their loan protfolio being 90% or greater LTV then a national decline of 10% (much less than the 25% haircut the Americans took) puts roughly $50 billion of CMHC insured mortgages underwater. Now of course not all of those people are going to default, but the point stands that the CMHC's portfolio certainly has the potential to have to be bailed out.

|

The taxpayer won't be on the hook until some outrageous real estate decline wipes out a ton of value and people start walking away from their houses en mass.

$50 billion of insured mortgages underwater doesn't put CMHC on the hook for $50 billion.

Underwater is meaningless. I've been underwater at some point. I didn't walk.

If I did walk, the bank would have taken back house, sold for a small loss and CMHC would be on the hook for the small loss. Not the full mortgage amount.

|

|

|

|

|

The Following User Says Thank You to ranchlandsselling For This Useful Post:

|

|

|

02-01-2012, 05:34 PM

|

#2028

|

|

First Line Centre

Join Date: Jun 2011

Location: Edmonton

|

Quote:

Originally Posted by albertGQ

They'd insure the entire 81%

|

I always thought that they only insured the first 20% and after that the banks trust that they have enough equity that they won't lose.

It struck me as wrong that on a $500k purchase you can put down 100k and they require no CMHC backing, yet if you are a little short (agreed to too many upgrades that raised the final price) and can only come up with 95k then they will charge you 5k to insure the loan.

|

|

|

|

|

02-02-2012, 08:02 AM

|

#2029

|

|

Franchise Player

|

Quote:

Originally Posted by GP_Matt

I always thought that they only insured the first 20% and after that the banks trust that they have enough equity that they won't lose.

It struck me as wrong that on a $500k purchase you can put down 100k and they require no CMHC backing, yet if you are a little short (agreed to too many upgrades that raised the final price) and can only come up with 95k then they will charge you 5k to insure the loan.

|

The premiums are based on the full mortgage amount, not the mortgage amount over 80%.

If you have CMHC insurance on it, your mortgage is insured for life.

Obviously, if you refinance conventionally, the insurance is gone

|

|

|

|

|

02-02-2012, 08:29 AM

|

#2030

|

|

The new goggles also do nothing.

Join Date: Oct 2001

Location: Calgary

|

Quote:

Originally Posted by macker

Hopefully Canada doesn't have to go through what has happened and is happening in the US but how can things be considered that much different here.

|

Because the bank lending rules here were never even close to what they had down in the US.

There's a vast difference between a 30 year vs 25 year mortgage and the reverse mortgages and stuff they had down there and had their debt service ratio requirements.

__________________

Uncertainty is an uncomfortable position.

But certainty is an absurd one.

|

|

|

|

|

02-02-2012, 08:52 AM

|

#2031

|

|

First Line Centre

|

Quote:

Originally Posted by photon

Because the bank lending rules here were never even close to what they had down in the US.

There's a vast difference between a 30 year vs 25 year mortgage and the reverse mortgages and stuff they had down there and had their debt service ratio requirements.

|

I am looking more from the standpoint of debt-to-income ratios and Canadians ability to service the loans. People have been saying this for years how Canada is so much safer/smarter/more secure/best banks in the world/different/stricter rules/should be the model for banks on a global basis etc.etc. If you look at things from the payer point of view and not the lender......debt to income over 150% etc.etc.

|

|

|

|

|

02-02-2012, 09:01 AM

|

#2032

|

|

First Line Centre

|

The Bank of Canada says that since the liquidity crisis of 2008-2009, household debt has increased at a rate that is twice the rate of the increase in disposable income.

There is nothing wrong with the Canadian banking system......it is Canadian household debt that is the problem......When mortgages are added to the debt picture the average Canadian household debt is $176,461 for an average household with two children. Compare this with the average family debt of $56,800 in 1990. Stats are from a CGA study....

|

|

|

|

|

02-02-2012, 09:35 AM

|

#2033

|

|

The new goggles also do nothing.

Join Date: Oct 2001

Location: Calgary

|

A broad stat of all people having increased debt doesn't equate to a mortgage crisis like the US had.

Debt is high, but in getting that debt people still had to have complied with the debt servicing ratio requirement.

I'm not saying it's a good thing to have all that debt, but we aren't facing a situation like the US had where they were giving out mortgages that depended on property value increasing otherwise the mortgage increased over time, or giving mortgages to people with a debt service ratio of inifinity because they had no income.

__________________

Uncertainty is an uncomfortable position.

But certainty is an absurd one.

|

|

|

|

|

02-02-2012, 09:46 AM

|

#2034

|

|

Lifetime Suspension

|

Canadians debt is somewhat offset by the assets they bought with it (real estate). The 'paper' net worth is still respectable.

When/If those assets tumble it will cause an ugly scenario.

Read on redflagdeals that TD LOC interest rates are going up. Some in the tune of 4% in addition to the 6% they were already paying.

Not cheap debt anymore.

|

|

|

|

|

02-02-2012, 09:56 AM

|

#2035

|

|

Scoring Winger

|

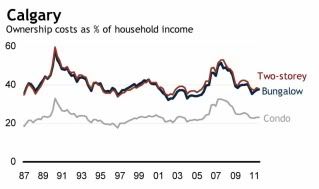

Here is an info graphic from a RBC report outlining Calgary homeownership costs over the past ~25 years. Seems that Calgary housing is more affordable now then lots of those past years (currently more "affordable" then the 25 year average).

http://www.rbc.com/newsroom/pdf/HA-1125-2011.pdf

http://www.rbc.com/newsroom/pdf/HA-1125-2011.pdf

Last edited by Suave; 02-02-2012 at 12:41 PM.

Reason: Had in the wrong years

|

|

|

|

|

02-02-2012, 10:11 AM

|

#2036

|

|

Franchise Player

|

Quote:

Originally Posted by Red

Canadians debt is somewhat offset by the assets they bought with it (real estate). The 'paper' net worth is still respectable.

When/If those assets tumble it will cause an ugly scenario.

Read on redflagdeals that TD LOC interest rates are going up. Some in the tune of 4% in addition to the 6% they were already paying.

Not cheap debt anymore.

|

Wait what? 10% in total?

|

|

|

|

|

02-02-2012, 10:38 AM

|

#2037

|

|

My face is a bum!

|

Quote:

Originally Posted by Suave

|

That doesn't line up with anything I've looked up on the subject, ever. If accurate, awesome. I don't think a housing crash can make anyone all that happy, even if they predict it and don't own any real estate.

|

|

|

|

|

02-02-2012, 10:44 AM

|

#2038

|

|

Lifetime Suspension

|

Quote:

Originally Posted by chemgear

Wait what? 10% in total?

|

Yes. Not sure about the rules of this site so I am not going to link, but from what I saw some people have 10%+ LOCs.

|

|

|

|

|

02-02-2012, 10:47 AM

|

#2039

|

|

The new goggles also do nothing.

Join Date: Oct 2001

Location: Calgary

|

Quote:

Originally Posted by hulkrogan

That doesn't line up with anything I've looked up on the subject, ever. If accurate, awesome. I don't think a housing crash can make anyone all that happy, even if they predict it and don't own any real estate.

|

Really? Affordability is something I've followed for years and Calgary's been quite good compared to other "high priced" places while I've watched it.

__________________

Uncertainty is an uncomfortable position.

But certainty is an absurd one.

|

|

|

|

|

02-02-2012, 11:03 AM

|

#2040

|

|

My face is a bum!

|

I guess I might not have ever found anything Calgary specific for housing vs income, just Canada wide, and then Calgary housing price history on it's own.

|

|

|

|

Posting Rules

Posting Rules

|

You may not post new threads

You may not post replies

You may not post attachments

You may not edit your posts

HTML code is Off

|

|

|

All times are GMT -6. The time now is 12:38 AM.

|

|